Author: Hubtel

KFC Marina Mall Receives Mobile Money And Bank Cards As Payment Options

February 26, 2018 | 1 minute read

KFC Marina Mall has joined the trail of businesses that use Hubtel POS to power their payments. Anyone can now order any KFC pack and pay using Mobile Money or a Ghanaian-issued Bank Card. This is good news for both KFC and their clients. Hubtel POS is a more convenient way to receive payments in your shop or store.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

Imagine paying for your next KFC order using any mobile wallet or bank card. That is just how KFC receives payment now using Hubtel POS. Your customers need a better way of making payments to you in your store. Use Hubtel POS and experience a new kind of payment.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

Jinlet pharmacy has become part of the growing number of businesses using Hubtel POS. We had the great privilege of setting them up. Signing up on Hubtel POS has helped create more convenience for their customers to pay either with a mobile money wallet or any Ghanaian issued bank card. Rethink how you accept payments from your customers with Hubtel.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

Smart gadgets are everything these days, and Hisense has them all. By using Hubtel POS, Hisense now allows you to buy all your favorite gadgets using any mobile wallet or Ghanaian-issued bank card. Hubtel POS provides Hisense a better way to receive payment as a business and a more convenient way for their customers to make payments.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

Let your customers pay you using any mobile wallet or Ghanaian-issued bank card. It is convenient for both you and your customers. Boulevard Menswear just joined the club. They accept all forms of payment because they signed up on Hubtel POS. Rethink your customers’ payment experience with Hubtel.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

With the help of Hubtel POS, Ramie’s Pub and Lounge has given their customers the option to pay from either any mobile wallet or a Ghanaian-issued bank card. They recently signed up and are already enjoying the benefits of using Hubtel POS.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

The time is 4:30am Monday morning and the signs on the doors of most banks in Ghana will read “Closed”. Yes, the “brick and mortar” bank at the corner of the busy road is closed, but not your mobile phone, not your telecom network, not your mobile money which you carry in your pocket wherever you go. With a smile on your face, you can stare at that sign reading “closed” and yet get the chance to transfer the funds to your son in university who needs to purchase that textbook tomorrow. Mobile money has caused a stir in traditional banking in Ghana in the last 5 to 10 years, and like it or not, its impact would be greatly felt.

Just as every new idea and improved ways of doing things comes with its own benefits and implications across various civilizations, cultures, and industries, the banking and financial sector in Ghana is currently experiencing another phase in its life through the Calvary charge of the “mobile phone” which is quickly sweeping over the country like a wildfire or a plague.

Financial inclusion: Out of every 10 Ghanaians about 4 of them have traditional bank accounts and only 3 may have their accounts active. The introduction of mobile money has given the banking industry the opportunity to reach out to the unbanked through their mobile phones. One can now open a traditional bank account even with a mobile phone. The days of needing to walk into a bank and fill out some forms are fast fading away. Currently, almost all telecom companies are making moves to synchronize one’s mobile money account with traditional banks in order to have ease of moving funds across accounts. This will expand the banking industry in terms of deposits through mobile money, and having a bank account could be as easy as dialing “1,2,3”

Cash-lite banking: Do you recall the smell of notes and money when you enter a typical banking hall? Or perhaps it is the sound of the money-counting machine. What about the “bam-bam” stamp sounds of the teller as she stamps the white band on the bank notes… All of these familiar things in traditional banks may be experienced less if mobile money continues to be successful in making the Ghanaian economy cash-lite. One may not need to carry thick wads of cash which may attract thieves as soon as one steps out of a banking hall. With the dawn of mobile money, hundreds of cedis can be wired across the nation without moving a foot. If mobile money gains more ground and capacity is built to handle bigger transactions and transfers, physical cash may exchange hands less often and traditional banks may equally be visited far less often.

General fear of unemployment: It is feared that with automation and making transactions electronic and convenient, fewer people may actually visit a traditional bank occasionally to make transfers or withdrawals. Introducing the automatic teller machine (ATM) saw a drop in walk-in clients making withdrawals. This move into automation and mobile money is speculated to cut down on the number of staff traditional banks may actually need for that aspect of operations (account opening, money transfers, and others) in the long run. However, mobile money has created thousands of employment opportunities for mobile money agents across the country. Traditional banks can equally innovate and provide core banking services to telecom firms that do not have banking as their core business. In the long run, traditional banking may move from being more staff to client related when mobile money takes over certain traditional frontline banking roles.

It is however important to note that with moves of merging mobile money accounts with traditional bank accounts through financial technology, your Mobile Money account may gradually be an extension of your traditional bank account, only this time, you will carry the “brick and mortar bank” in your pocket everywhere you go.

Related

Correction of False Claims About ECG Commercial Agreement

September 29, 2024| 6 minutes read

Gen Z vs Millennials: What are they ordering?

June 24, 2024| 2 minutes read

Hubtel Announces Completion of Commercial Agreement with ECG

March 28, 2024| 6 minutes read

In the past few years in Ghana, two popular words have surfaced when it comes to payments and they are “Mobile Money”. In a country where 7 out of 10 people are without bank accounts but yet have more mobile phones than people, (due to multi-sim users), what role can mobile play in impacting our nation’s growth and development?

Financial Inclusion: Between Circle and Adabraka, you are likely to come across 5 different banks yet only 3 out of 10 Ghanaians have bank accounts. The birth of mobile money along with the recent partnerships between banks and telcos in Ghana have made great strides in reaching the unbanked sections of society. Since 1 out of 5, Ghanaians use mobile money banking regularly, free movement of money in the economy that hitherto was hoarded by the unbanked and exchanged just a few hands will be enabled. The movement of money in the economy through mobile money banking will equally affect credit availability because these monies from mobile money transactions end up in the banks and work hand in hand with the telecom companies. The ability to link one’s mobile number to a traditional bank account may further encourage the unbanked to open bank accounts with the confidence that their monies will still be in their “pockets” in the form of a mobile wallet.

Micro Insurance penetration: With Ghana’s insurance penetration to GDP hovering a little below 2%, the use of mobile phones does not only have a place for banks but also a place for the insurance industry as well. In recent times, some telecom companies offer a form of microinsurance via mobile by providing life and health insurance covers to willing phone subscribers. This is made possible through agreed and controlled data sharing between telecom firms and traditional insurance companies who underwrite the policies. One can send a message to a short code and pay a flat rate per month through a direct mobile money monthly debit and enjoy health insurance or life cover. This innovation in insurance in the mobile money sector puts in place a positive outlook for the future of insurance in Ghana. It will also help improve healthcare service delivery in the nation if millions subscribe to this coverage monthly. Imagine 20 million phone users signing on to a minimum GHS5 a month for a GHS1000 hospital bill cover. The income generated by these subscribers will be at least GHS100 million a month and at least GHS1.2 billion a year. If the mathematics of the fund is managed well by actuaries using good data, mobile money could rejuvenate life and health insurance in Ghana. These funds could equally be invested and turned around to earn higher returns in order to positively stabilize the economy.

Employment: The impact of mobile money on employment is a blessing and curse, but more of a blessing. With increased automation of money transactions, certain roles of traditional brick-and-mortar banks will grow dysfunctional, causing a possible retrenchment in areas that have been taken over by mobile and online banking. Imagine, where would the 72,000 mobile money agents littered across the country have been if the innovation of mobile money had never seen the light of day? The private sector through mobile money has hence helped the nation solve the menace of unemployment to a degree.

Tax revenue generation for the State: The government of Ghana relies on funds from various sources in national development and one of these is tax. The generation of transactional taxes from money transfers, corporate taxes from telecom firms, and income tax from commissions of mobile money agents all help drive the developmental agenda of the nation. This is a positive impact indeed for a developing nation like Ghana. One can be assured every successful transaction done via mobile money contributes a quota to national development through tax.

Avenue for financial cybercrime: We cannot speak about the positive impact of mobile money without the threats it also presents. One such key threat is the avenue mobile money creates for financial cyber fraud. Lately, issues of fraudsters hacking or attempting to hack into mobile money subscribers’ accounts are becoming a menace. People of ill motives are devising various means of getting subscribers’ passwords and some successful cases result in huge aggregate sums of money. This issue of mobile money fraud can in the end lead to mistrust of the financial platform and it could result in the possible collapse and lack of interest in the mobile money sector if firm steps are not taken. Because risk presents an opportunity, cyber and financial risk experts can equally take advantage of this to serve as consultants in telecom firms to ensure the financial integrity and safety of the mobile money subscriber are maintained.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

In the early 2000’s, researchers found out that some mobile phone users would sell their airtime to friends and family for cash. This clever, but improvised use of airtime as a substitute for money transfer was the precedent on which mobile money was created.

Over the years, mobile money in Ghana has seen significant development because of the many advantages it carries. The service, which was introduced in Ghana in 2009 by Ghana’s leading Telecommunications Company MTN is now offered by tiGO, Airtel and Vodafone. In fact, one out of every five Ghanaians has a mobile money account.

Setting up a mobile money account is fairly easy. Once you have a valid national ID card and a SIM card, you just visit your network provider and an account will be created and linked to your mobile number. The only thing you need to make transactions is your PIN number. Fin. Comparing this with traditional banking, where you would actually have to walk into banking hall, fill out documents, make a minimum deposit and walk out with a cheque book and an ATM, it is easy to understand why many Ghanaians are opting for mobile money instead.

The fact that there are many mobile money agents in Ghana makes it easier and more convenient when you have to withdraw money. Let’s say you live and work in Kumasi and need to transfer some money to your sister in a village. Before the onset of mobile money, you may have had to transfer the money through someone, say a friend or a distant relative. This comes with some delay and risk of your sister receiving less than expected. But with mobile money, no matter which network you use, there is at least one agent who can assist your sister cash out almost immediately you transfer the cash.

Gone are the days when local traders would ply long distances without fear of being robbed of valuables by armed bandits in the middle of their journey. Rather than carrying large amounts of money and hoping for event-free trips, more and more traders now transferring money to their mobile money accounts, travelling light and redeeming their money when they arrive safely at their destination.

Even though there has been a mass adoption of the service, Ghanaians primarily use the service for cash in/cash out transactions. They do not use mobile money to pay for utilities and make other online purchases as is the norm in Kenya and Tanzania. This indicates that the service is guaranteed to get better as companies begin to take advantage of the unique opportunities opened up by mobile money. Hubtel, for one, offers a Point of Sale (POS) software for businesses who have products or services to sell and want to give their customers the convenience of paying with a variety of payment options including mobile money.

With the burgeoning and innovative use of the service, mobile money in Ghana is guaranteed to continue rising. Who knows, it could even disrupt traditional banking.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

Hubtel Joins 30-year-old’s GHc87,000 Fundraising Bid To Help Him Walk Again

October 3, 2017 | 3 minutes read

Ever since we at Hubtel heard Baffour Awuah Tabury’s touching story on Citi FM, we have made it one of our 2017 goals to “Make Baffour Walk Again.”

Before everything changed on the road to realizing his dreams and making his mother proud, Baffour was a final-year student at the University of Cape Coast and getting ready to graduate. He was involved in a motor accident that left him paralyzed from his waist down in 2007. Due to this unfortunate turn of events, Baffour had difficulty controlling his urine and bowels. Like any loving and caring mother will do, Baffour’s mum resolved to do everything in her power to see her son walk again. This included burning over GHS 200,000 of her personal savings and investments on various procedures and two surgeries in Ghana. Last year, Baffour successfully had another surgery in China which restored his urinary and bowel control.

For Baffour to walk again, the next step will be to undergo physiotherapy at NextStep Orlando (no pun intended). This physiotherapy center in Orlando, Florida treats patients who have injured their spinal cords so they can fully recover their functions. Amazing right? Yes, but this procedure will cost a cool GHS 87,000 ($19,200). And this is where Hubtel comes in.

We have developed a Point of Sale platform called the Hubtel POS. This platform is tailored to allow businesses to accept payments and charity organizations to receive funds from all mobile money wallets and bank cards in their stores, online, or on the go into one account. With our POS, we eliminate the burden of having to hold four different phone numbers to receive payments. Making it easier for everyone who is touched to help resolve situations like Baffour’s, to make a donation to help Baffour walk again.

So now how do I donate to this cause? It’s simple – just dial *713*7140# on your phone – it doesn’t matter which network you’re on, follow the instructions, and make a donation. Think of it this way: if 8,700 individuals make a donation of GHS10, Baffour’s dream of walking again will be realized.

Hubtel has not only provided this shortcode to ease Baffour’s access to donations for his surgery, we are also waiving all network charges associated with mobile money transfers made to this donation.

So go ahead. Dial *713*7140#, and let’s make Baffour walk again!

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

Credit to Cedi

We at Hubtel are obsessed with finding ways to simplify our pricing, and we have great news. We are making two changes that make your Hubtel experience a lot better.

Firstly, the value of your top-up has previously been displayed as the number of messaging credits. Starting Sunday, 1st October this will now be shown as currency balance in Cedi, or Dollars in your account.

Bundles

Second, we have introduced some great value bundles for you to make significant savings. Campaigns that you run when you have not paid for a bundle will be charged at a flat standard rate of 0.03 for local messages.

Your new bundles give you up to 40% savings! Choose the monthly or quarterly bundles that best suit your needs.

Before the end of the bundle period, you can roll over your remaining value by buying another bundle or allowing your current bundle to expire. Your main currency balance will not expire so you can always buy more value bundles whenever you are ready.

Log into your account to purchase any of our nearly 40% cheaper bundles. If you need help or want more information we are always just a call or email away. Just call us toll-free on 0800 222 081.

Related

Hubtel and Alex Bram Earn Double Nominations at Ghana AI Awards 2025

March 26, 2025| 2 minutes read

Hubtel Attains ISO 27001:2022 Certification

February 24, 2025| 2 minutes read

Celebrating Leadership: Alex Bram Awarded EMY 2024 "Man of the Year – Technology"

December 31, 2024| 2 minutes read

Since we relaunched as Hubtel we have been offering the lowest bulk SMS messaging rate through our new bundles.

To enable us offer the same competitive rates on other services such as USSD, toll-free SMS, and payments, we are making some important changes from this weekend.

Starting this Sunday, 1st of October 2017, we are changing our credit-based balance to a currency-based balance.

This means if you had 380 SMS credits you will now see it as a balance in your local currency (e.g. Ghc10) on your account.

From this currency balance, you can buy a corresponding SMS bundle.

If you need help or want more information we are always just a call or email away. Kindly call toll-free number 0800 222 081.

#RethinkCustomerService

Related

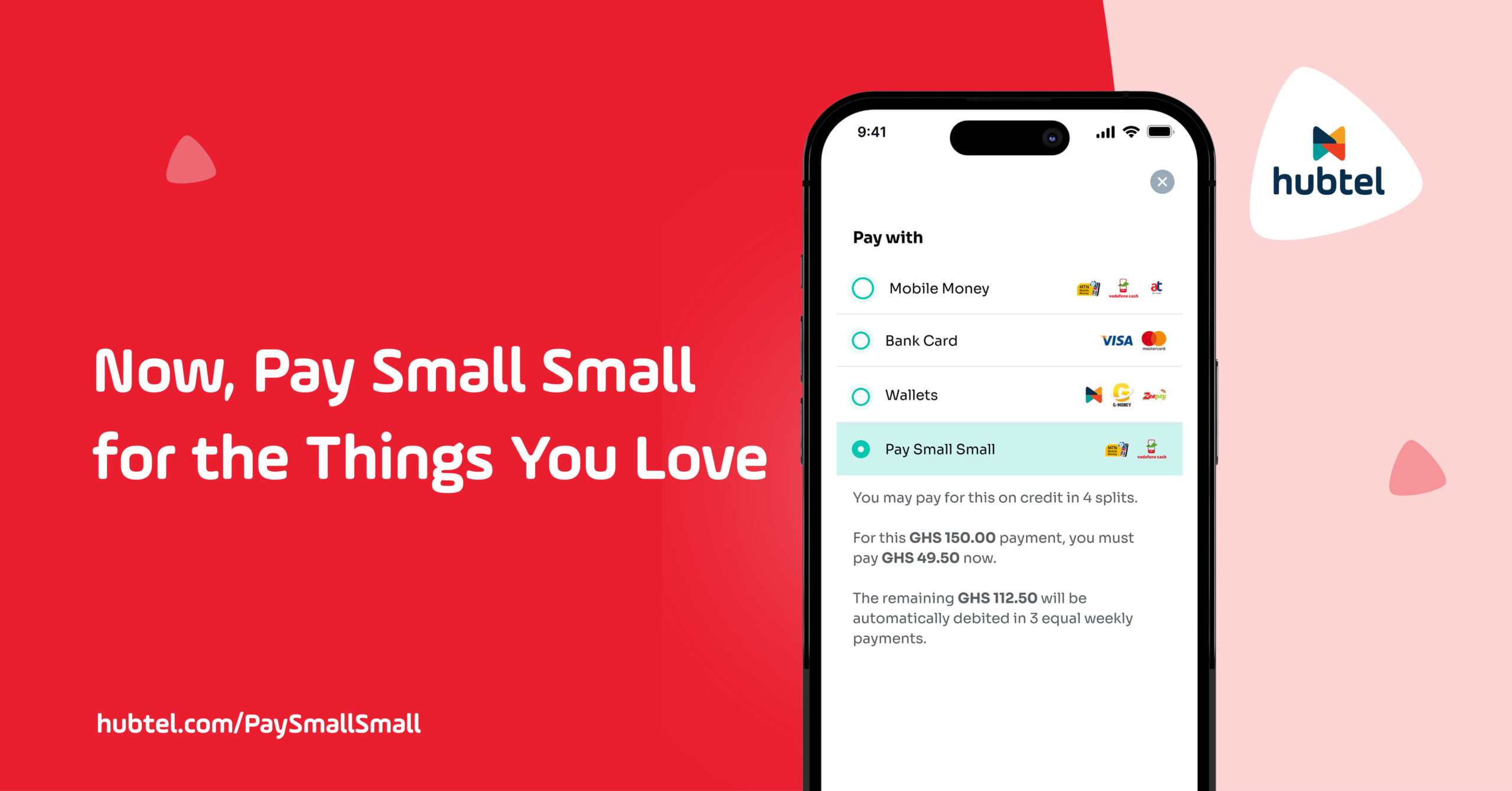

Now, Pay Small Small for the Things You Love

December 23, 2024| 2 minutes read

Hubtel Completes Biggest Upgrades to Developer Portal

July 24, 2024| 3 minutes read

Gen Z vs Millennials: What are they ordering?

June 24, 2024| 2 minutes read